【專題演講】113/06/06(四) 15:30-16:30 Jiun-Hua Su Ph.D. 蘇俊華 研究員

Abstract

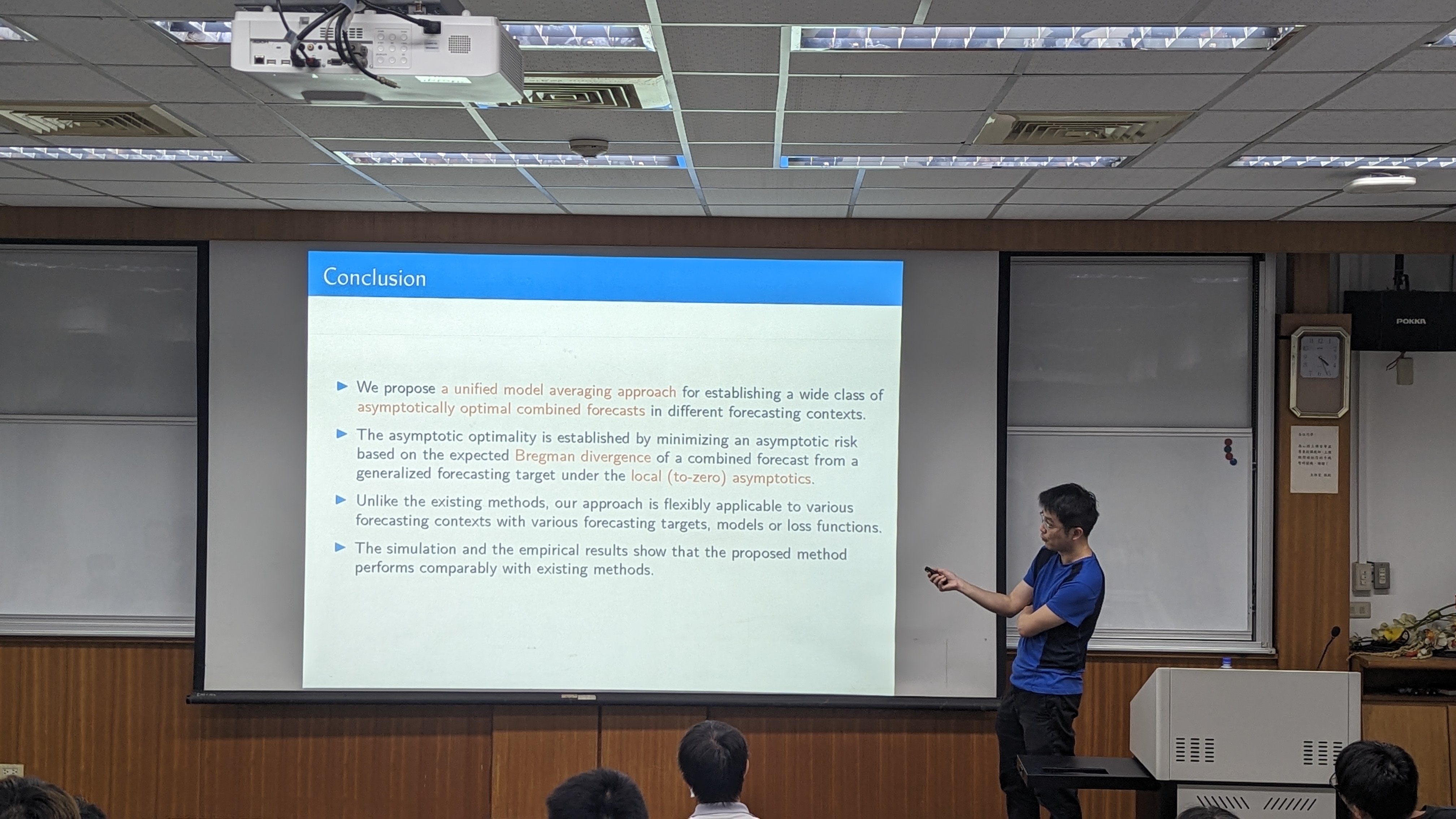

We propose a unified model averaging (MA) approach and establish its asymptotic optimality for a wide class of forecasting targets. The asymptotic optimality is achieved by minimizing an asymptotic risk based on the expected Bregman divergence of a combined-forecast sequence from a forecasting-target sequence under the local(-to-zero) asymptotics. This approach is flexibly applicable to generate MA methods in different forecasting contexts, including, but not limited to, univariate or multivariate mean forecasts, volatility forecasts, probabilistic forecasts and density forecasts. We also conduct Monte Carlo simulations (empirical applications) to show that compared to related existing methods, the MA methods generated by this approach perform reasonably well in finite samples (real data).